The journey into real estate investing often begins with understanding the numbers. In the accompanying video, you witness a practical example of a successful rental property investment, purchased over a decade ago, and how it has generated both monthly cash flow and significant appreciation. This real-world scenario illustrates the potential for building wealth and achieving passive income through strategic property acquisition.

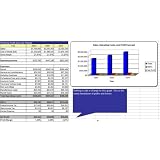

When considering a rental property, it’s crucial to break down the financial components from the initial outlay to ongoing expenses and long-term gains. The video highlights a property bought for $241,000 in 2012, which has since more than doubled in value, now estimated at $504,000. Such growth underscores the power of long-term real estate holdings.

Deconstructing the Initial Investment in a Rental Property

Embarking on your first rental property investment requires a clear understanding of the upfront costs. These expenses go beyond just the purchase price, encompassing several key components that form the foundation of your investment.

Understanding Your Down Payment

The video example details a 25% down payment on the $241,000 property, totaling $60,250. This percentage is common for investment properties, as lenders often require a larger equity stake compared to owner-occupied homes. A substantial down payment not only reduces your loan amount but can also lead to more favorable interest rates over the life of the mortgage.

Accounting for Closing Costs

Beyond the down payment, closing costs are an essential part of the initial investment. The investor in the video allocated an additional sum for these fees, which typically range from 2-5% of the property’s purchase price. These costs cover various services and fees associated with finalizing a real estate transaction, including appraisal fees, title insurance, attorney fees, loan origination fees, and recording fees. Neglecting to budget for these can derail an otherwise sound financial plan.

Budgeting for Renovations and Upgrades

Many investment properties, especially first purchases, benefit from initial renovations. The video mentioned $13,000 invested in upgrades, a wise move to enhance the property’s appeal and rental value. Renovations can increase the rent you can charge, attract higher quality tenants, and potentially accelerate the property’s appreciation. It is paramount to plan these expenses thoughtfully, aiming for improvements that offer a strong return on investment.

Calculating Monthly Cash Flow: Income vs. Expenses

The true measure of a profitable rental property often lies in its monthly cash flow. This involves a careful calculation of all income generated against all recurring expenses. Positive cash flow means your property is generating profit each month after all bills are paid, contributing to your goal of passive income.

Rental Income: The Primary Revenue Stream

The core of any rental property’s income is the rent collected from tenants. In the video, the property generates $2,050 per month. Establishing a competitive rent requires thorough market research, evaluating comparable properties in the area, and considering the condition and amenities of your specific unit. Setting the right rent ensures consistent occupancy and maximizes your returns.

Managing Property Management Fees

For investors seeking a truly passive income stream, professional property management is a common choice. The video highlights an 8% property management fee, which amounts to $164 per month from the $2,050 rent. This fee typically covers services like tenant screening, rent collection, maintenance coordination, and legal compliance. While it reduces your gross income, it frees up your time and expertise, making the investment much more hands-off.

Essential Monthly Expenses: Mortgage, Taxes, and Insurance

Subtracting all expenses from the rental income reveals the net cash flow. The video breaks down these critical monthly outflows:

- Mortgage: $870 per month. This covers the principal and interest payment on the loan used to purchase the property. Understanding how much of this goes towards reducing your principal versus interest is key to tracking equity growth.

- Property Taxes: $290 per month. Property taxes are levied by local governments based on the property’s assessed value and fund public services. These can vary significantly by location and typically adjust over time.

- Homeowners Insurance: Approximately $50 per month. For a rental property, you will need a landlord policy, which differs from standard homeowners insurance. It provides coverage for the building itself, liability protection, and potential loss of rental income due to covered perils.

Factoring in Unforeseen Costs: Repairs and Vacancies

While the video’s investor enjoyed a period of minimal repairs and vacancies, it is prudent for any new investor to allocate funds for these potential costs. Unexpected expenses can quickly erode profits if not properly planned for.

Allocating for Repairs and Maintenance

The speaker in the video suggests hypothetically allotting 10% for repairs and vacancies. This is a common rule of thumb among investors. Regular maintenance is crucial for preserving your property’s value and keeping tenants happy, but unforeseen issues like a leaking roof or a broken appliance can arise. Setting aside a percentage of your rent each month in a separate fund ensures you are prepared for these eventualities without impacting your personal finances.

Minimizing Vacancy Periods

A vacant property generates no income but still incurs expenses like mortgage payments, taxes, and insurance. The investor’s success in avoiding many vacancies highlights the importance of good property management and maintaining a desirable property. Strategies to minimize vacancies include thorough tenant screening, responsive maintenance, and setting market-competitive rent. Even short vacancy periods can significantly impact your annual returns, making proactive management essential.

The Long-Term Gain: Property Appreciation and Equity

While monthly cash flow is vital, the long-term value appreciation of a rental property often constitutes a significant portion of an investor’s total return. The video’s example vividly demonstrates this aspect of real estate investing.

Understanding Market Appreciation

The property, purchased for $241,000 in 2012, is now valued at $504,000 according to Zillow, showcasing an impressive appreciation of over $260,000 in eight years. This growth is influenced by various factors, including local economic growth, population trends, inflation, and development in the surrounding area. Investing in a growing market or an area undergoing revitalization can significantly boost your property’s long-term value.

Building Equity Over Time

Beyond market appreciation, investors also build equity as they pay down their mortgage. A portion of each mortgage payment goes towards reducing the principal, steadily increasing your ownership stake in the property. This combination of principal reduction and market appreciation contributes to substantial wealth accumulation over time. The video’s investor, having held the property for eight years, has undoubtedly benefited from both these aspects, illustrating the power of patient, long-term real estate investing.

The example shared in the video clearly demonstrates the potential for profitability and wealth creation through a well-managed rental property investment. By carefully analyzing initial costs, managing monthly income and expenses, and understanding the long-term benefits of appreciation, aspiring investors can confidently embark on their own journey into real estate.

Unpacking Your Property Profits: Q&A

What is a rental property investment?

A rental property investment involves buying a property and renting it out to tenants. The goal is to earn monthly income and potentially see the property’s value increase over time.

What initial costs should I expect when buying my first rental property?

Beyond the property’s price, you’ll need a down payment (often 25% for investment properties), closing costs (which cover fees like appraisal and title insurance), and sometimes funds for initial renovations.

How does a rental property create monthly profit or “cash flow”?

Monthly cash flow is the money remaining after you subtract all your regular expenses, such as mortgage payments, property taxes, insurance, and property management fees, from the rent you collect.

How does investing in a rental property help me build wealth in the long run?

You build long-term wealth in two main ways: through property appreciation, where the property’s market value increases over time, and by building equity as you pay down your mortgage.